.avif)

.avif)

Ready to invest in AI?

Schedule time with Zeni's finance pros to learn more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Series D funding rounds often provide the capital startups need to delay an exit or continue operating privately at scale.

In this guide, we explore our unique research on Series D companies in 2026, including average fundraising amounts, headquarters locations, industry representation, and drop-off rates from Series C.

Among companies that raised Series D funding between May 20, 2025, and May 20, 2026, the average round size was roughly $210.5 million. That’s a striking increase of 88% from the $111.9 million average seen during the 2025 calendar year.

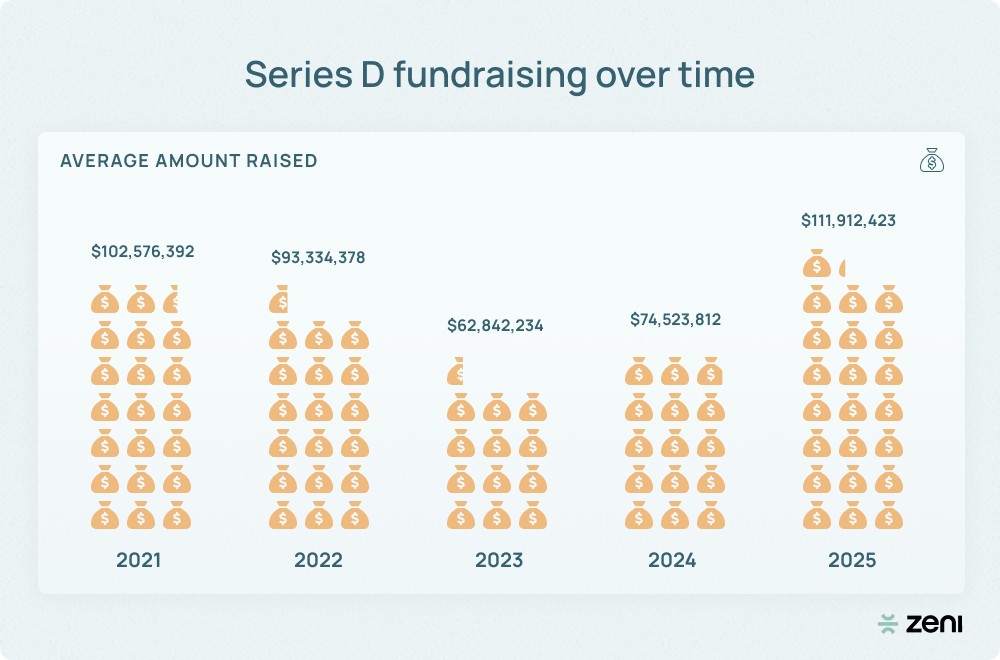

This shows continued momentum after several difficult years for venture capital markets. Following a post-2021 decline that pushed the average Series D funding round down to $62.8 million in 2023, funding levels have been recovering since 2024.

However, median Series D fundraising amounts tell a more restrained story. They’ve yet to recover from their $80 million peak in 2021, sitting at $55.8 million in 2025 and roughly $72.8 million in the 12-month period ending May 20, 2026.

This suggests that the recent jump in average Series D fundraising amounts is heavily skewed by a relatively small number of massive rounds, primarily concentrated in and around the booming artificial intelligence (AI) industry.

The most significant example is Waymo, the autonomous driving company headquartered in Mountain View, California. In February 2026, the company raised an enormous $16 billion Series D round.

Another outlier is Anysphere, the San Francisco-based company behind the AI coding platform Cursor. The startup raised approximately $2.3 billion in Series D financing, capitalizing on strategic investors’ enthusiasm for generative AI developer tools.

A third major raise came from Saronic, an Austin-based defense and autonomous maritime vehicle company. At the end of March 2026, the startup secured roughly $1.75 billion in Series D funding, highlighting growing interest in military applications of AI.

Total funding amounts for Series D companies also reached record levels between May 20, 2025, and May 20, 2026, with the average company raising $417.3 million overall by the time it completed its Series D round.

For context, the previous high came in 2021, when the average total funding amount reached $216.7 million. Even during the stronger 2025 calendar year, the figure sat far lower at approximately $266 million.

Median trends once again paint a more moderate picture. After peaking at $141.5 million in 2022 and falling to $116.7 million in 2023, they recovered to $161.9 million in 2025 before reaching $184.8 million in the 12-month period ending May 2026.

This is another reflection of averages being heavily influenced by a small number of unusually well-capitalized companies, primarily in AI and adjacent industries. That included the same startups that raised the biggest individual Series D rounds, namely:

Several additional companies also reached exceptional total funding levels during the period. These included Wayve, the London-based autonomous driving startup, which achieved $2.52 billion in total equity funding from institutional investors.

Meanwhile, both Ascend Elements and Cohere surpassed the $1.7 billion total funding at the tail end of 2025. Ascend Elements manufactures sustainable battery materials, while Cohere develops enterprise AI software.

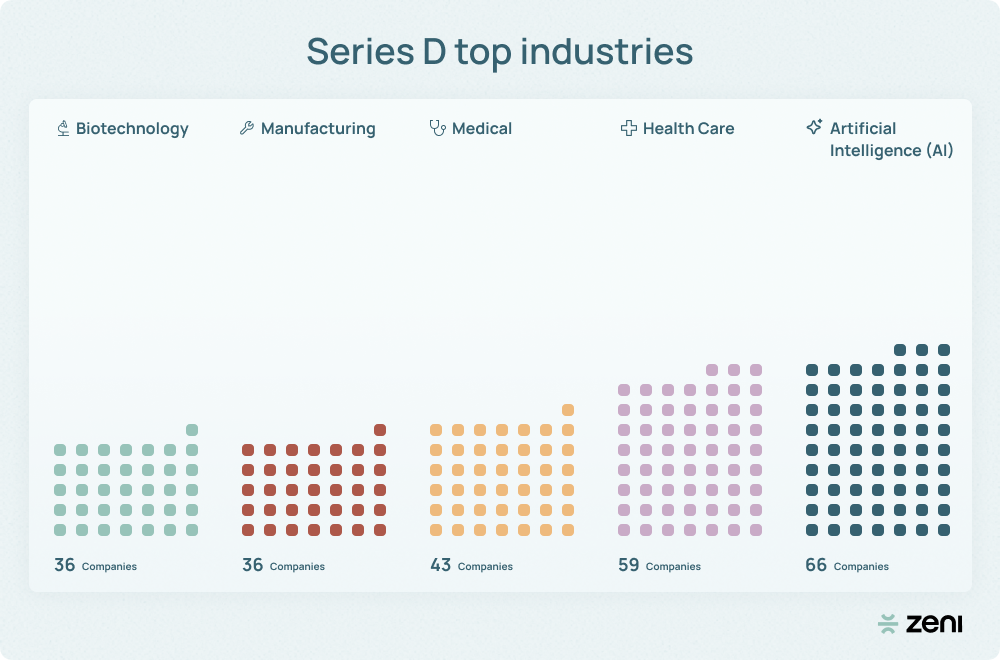

AI, healthcare, and medical companies dominated the Series D landscape between May 20, 2025, and May 20, 2026. However, manufacturing, biotechnology, and software companies also accounted for a substantial share of fundraising activity.

AI industry tags appeared in 26.6% of all Series D companies, making it the single most represented in the dataset. Healthcare followed closely behind at 23.8%, while medical companies accounted for 17.3%.

Investor interest in AI also likely contributed to the strength in the adjacent categories. Biotechnology and manufacturing companies each appeared in 14.5% of Series D startups, while software companies represented 14.1%.

At the sector level, Healthcare & Life Sciences ranked as the largest category overall, representing 34.3% of all Series D companies. Hardware, Semiconductors & Deep Tech followed closely behind at 33.1%, with Enterprise / B2B Software just after at 31.9%.

AI & Machine Learning also represented a large portion of venture capital activity at 26.6%, reinforcing how central the tech has become. Consumer & E-Commerce and Fintech & Financial Services maintained smaller but still notable shares.

These percentages don’t add up to 100% because many Series D startups operate across multiple industries simultaneously. For example, a single company may qualify as an AI, robotics, and enterprise software startup at the same time.

The United States remains the largest hub for Series D companies in the world. Of the companies we found in 2026, 107 are headquartered in the U.S., accounting for roughly 43.1% of the total dataset.

China ranks second with 64 companies, representing 25.8% of all Series D startups. Together, the U.S. and China account for nearly 69% of the companies in our analysis, highlighting how concentrated late-stage venture capitalist activity remains globally.

Japan and India each account for 17 Series D companies, while the United Kingdom and South Korea follow with eight apiece. Beyond those countries, representation drops off quickly, with most nations home to only a handful of companies.

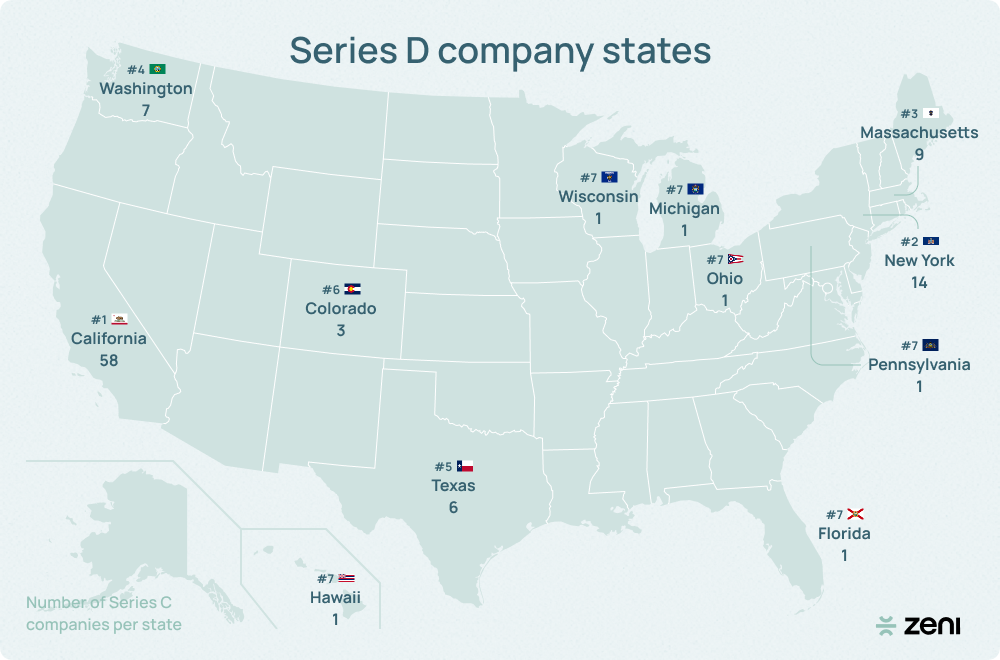

Within the United States, Series D activity is even more concentrated geographically. California alone accounts for 58 companies, representing more than half of all American Series D startups and nearly a quarter of the overall dataset.

New York ranks a distant second with 14 companies, while Massachusetts, Washington, and Texas round out the top five. Together, those states represent the overwhelming majority of U.S. Series D activity.

At the city level, San Francisco leads with 15 Series D companies, narrowly ahead of Beijing with 14 and Tokyo with 13.

Shanghai and New York are close behind, reinforcing the value of proximity to financial institutions like investment banks, private equity firms, and hedge funds.

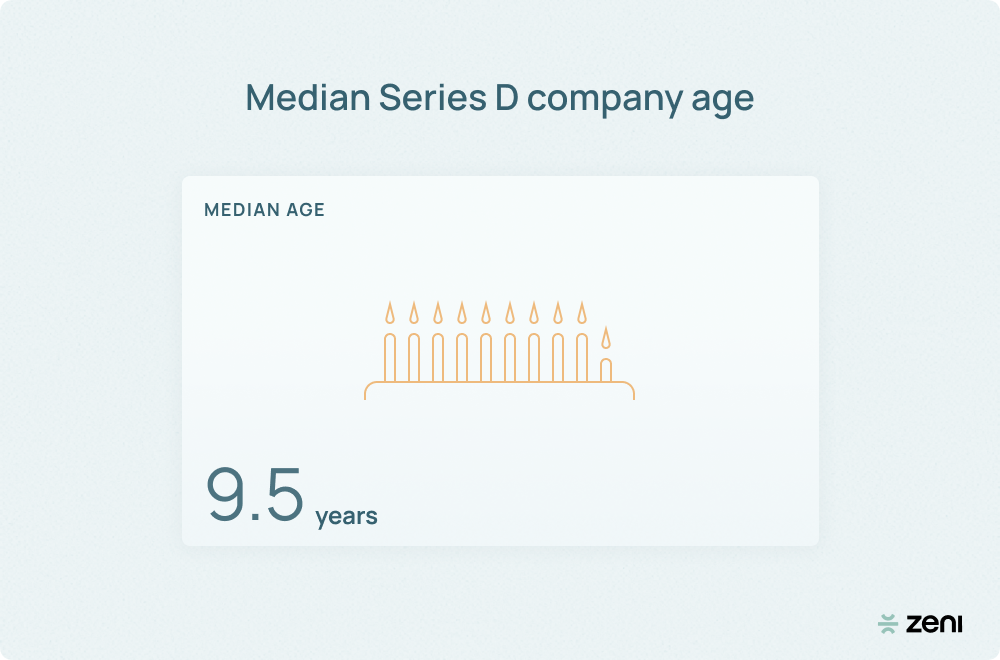

Based on a median founding date of January 1, 2016, among Series D companies in our 2026 dataset, it takes approximately 9.5 years of growth to reach the Series D startup funding round.

That’s notably longer than the median of 7.5 years that it takes to reach the Series C funding round. This is likely due to the difficulty of raising additional capital beyond Series C and the broader trend of startups remaining private for longer periods.

In practice, series funding timelines vary significantly depending on industry and business model. For example, software startups can often scale quickly through seed funding, Series A funding, and Series B funding due to lower capital requirements.

Meanwhile, biotechnology and autonomous systems companies may require years of research and infrastructure development to reach maturity, potentially reaching a Series E funding round or even the Series F funding stage.

The number of companies reaching Series D drops sharply compared to Series C. In the period between May 20, 2025, and May 20, 2026, we identified 604 Series C companies but only 248 Series D companies.

That represents a decline of nearly 59%, likely reflecting both the common goal of pursuing an exit around the Series C round and the increasing difficulty of raising capital at later startup funding stages.

The composition of the market also changes meaningfully between the two stages. AI companies accounted for roughly 42% of disclosed Series C funding dollars but nearly 64% at the Series D stage.

This suggests that Series D investors and capital firms increasingly focus on a smaller group of perceived AI leaders as companies mature. Median AI fundraising amounts also climb from roughly $80 million at Series C to $100 million at Series D.

Geographic representation shifts at Series D as well. U.S.-based companies accounted for 39.2% of Series C startups in our dataset but 43.1% of Series D companies.

Meanwhile, Asia’s share fell modestly, indicating that American startups may currently face an easier path to securing very late-stage venture financing.

There were also notable differences in sector composition. Enterprise and B2B software companies represented the largest category at Series C, while Healthcare & Life Sciences became the leading sector at Series D.

That likely comes from the longer timelines common in biotech, medical, and pharmaceutical industries, where companies often require additional late-stage funding before reaching an initial public offering (IPO) or strategic acquisition.