.avif)

Ready to invest in AI?

Schedule time with Zeni's finance pros to learn more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

In our 2026 Accountant AI Survey, Zeni conducted independent research through a survey of 100 accounting professionals, including public accountants, in-house accountants, and finance leaders.

In this research report, we review the results of the survey, supplementing our analysis with key accounting statistics from Bureau of Labor Statistics (BLS) data, AICPA Trends Reports, and NASBA licensing figures.

According to the most recent BLS.gov data, there were 1,579,800 accounting and auditing jobs in the United States as of 2024. The Bureau of Labor Statistics (BLS) also expects that number to grow roughly 5% by 2034, reaching a total of 1.65 million.

This outpaces the projected 3% average growth for all occupations over the same time period. It also translates to about 124,000 accounting job openings each year on average as workers switch to different occupations or exit the workforce.

According to the Accountancy Licensee Database, 653,408 accounting professionals were also active Certified Public Accountant (CPA) license holders as of August 2025, not including those in Hawaii or New Mexico.

This means that approximately 40% of accountants in the United States hold an active CPA license. In other words, fewer than half of accounting professionals have fulfilled the requirements to maintain the industry’s gold standard credential.

This number has remained surprisingly consistent over the years. For example, while the number of auditing and accounting jobs was 1.28 million in 2019, the number of licensed CPAs was 654,375.

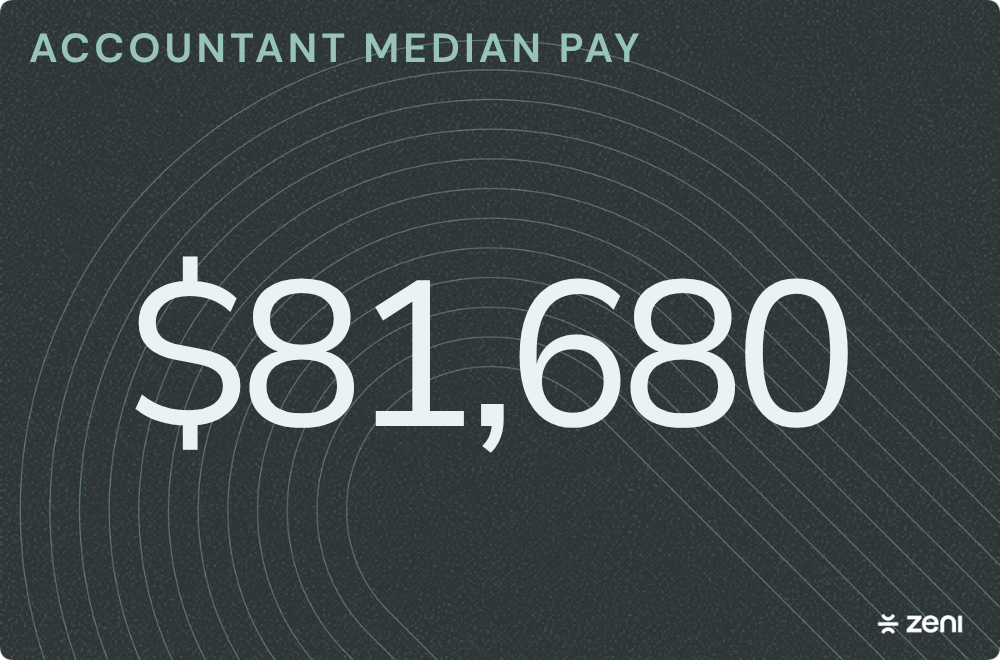

BLS wage statistics show that the median annual income for accountants was $81,680 in 2024. However, earnings vary widely across the profession. The lowest-earning 10% took home $52,780 that year, while the highest-earning 10% made more than $141,420.

In practice, the specific type of accounting services a professional provides plays a big role in where they fall along this scale. The BLS found that median annual wages for accountants were highest in the following industries:

In addition to industry, factors like job title, years of experience, and location can also have a significant impact on an accounting professional’s compensation.

For example, Corporate Controller salaries range from around $152,000 to $213,250 across the U.S. However, in Los Angeles, accounting salaries are 31% higher than the national average, shifting the range to between $199,120 and $279,358.

Meanwhile, the national average for Senior Accountants ranges from $80,000 to $109,000, but drops to $72,000 to $98,100 in Dayton, Ohio, where salaries are approximately 10% lower.

Many signs point to an ongoing accountant shortage in the U.S. While demand for talent continues to grow, the number of graduates entering the accounting profession has been shrinking for years.

According to the AICPA's 2025 Trends Report, 75% of leading accounting firms that hired accounting graduates in 2024 planned to hire the same number or more in 2025.

However, the number of students graduating with accounting degrees has fallen steadily from 78,518 in the 2017–2018 academic year to 55,152 in 2023–2024. This represents a year-over-year decrease of 5.7% and a total decline of almost 30%.

The accounting field experienced a similar decline in unique CPA candidates over the same period. While there was a temporary increase ahead of the CPA Exam's 2024 restructuring, the figure fell from 39,436 in 2017 to 28,082 by 2024.

More alarmingly, the AICPA estimates that 75% of CPAs are Baby Boomers that will probably retire within the next 10 years. This is called the “Silver Tsunami”.

Our survey findings echo this trend. Of the 100 accounting professionals we surveyed across CPA firms and finance departments, 60% said it has been somewhat or very difficult to hire qualified accounting staff in 2026.

The accounting shortage may increase in the short term as the Baby Boomer generation reaches retirement age. Per the New York State Society of CPA’s State of the Profession Report, roughly 25% of current New York partners are now older than 60.

However, there are also some signs of the long-term trend reversing. In 2025, total enrollment in U.S. accounting programs hit 266,506 students, up 12.4% from 237,197 in 2024 and the highest it’s been since 2020.

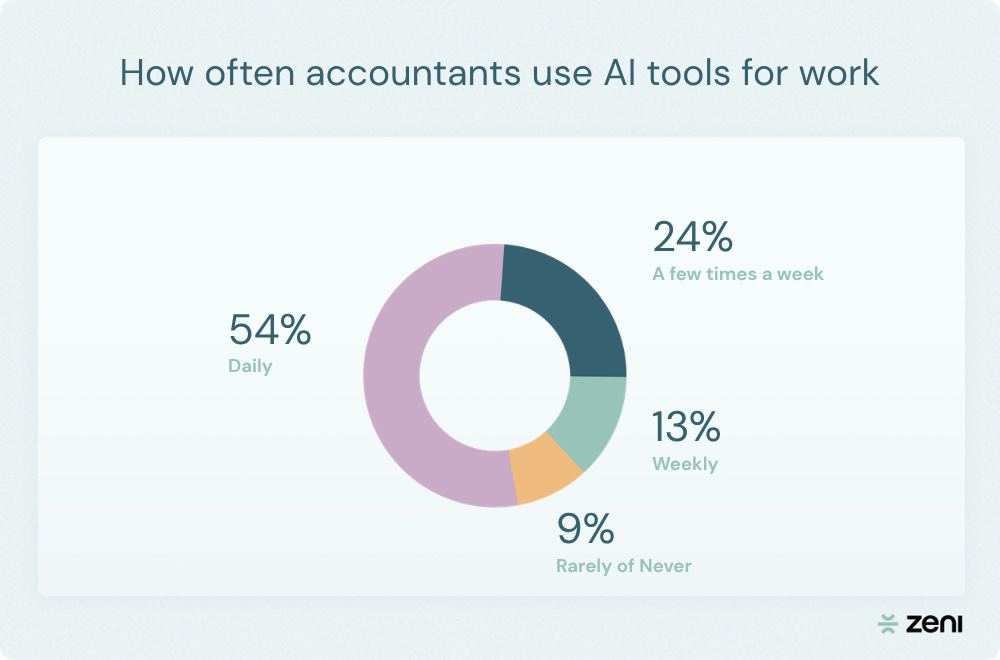

AI adoption has become all but universal among accounting professionals. In our survey of 100 accountants and finance leaders, 91% reported that they use AI tools at least occasionally. Only 5% said they don’t use AI and have no plans to start.

In addition, AI has largely moved beyond experimentation and into regular workflows. Over half of respondents (54%) said they use AI tools daily, while another 24% report using them several times per week. Combined, 91% reported using AI at least weekly.

General-purpose AI assistants—such as Claude, ChatGPT, and Gemini—remain the most common tool of choice. However, accountants are also increasingly branching out into more specialized solutions.

For example, more than half of respondents (51%) reported using AI features inside accounting software platforms, like Zeni’s AI accounting agent and AI CFO agent.

Another 38% said they use dedicated AI accounting or finance tools, while 18% reported working with custom in-house AI systems.

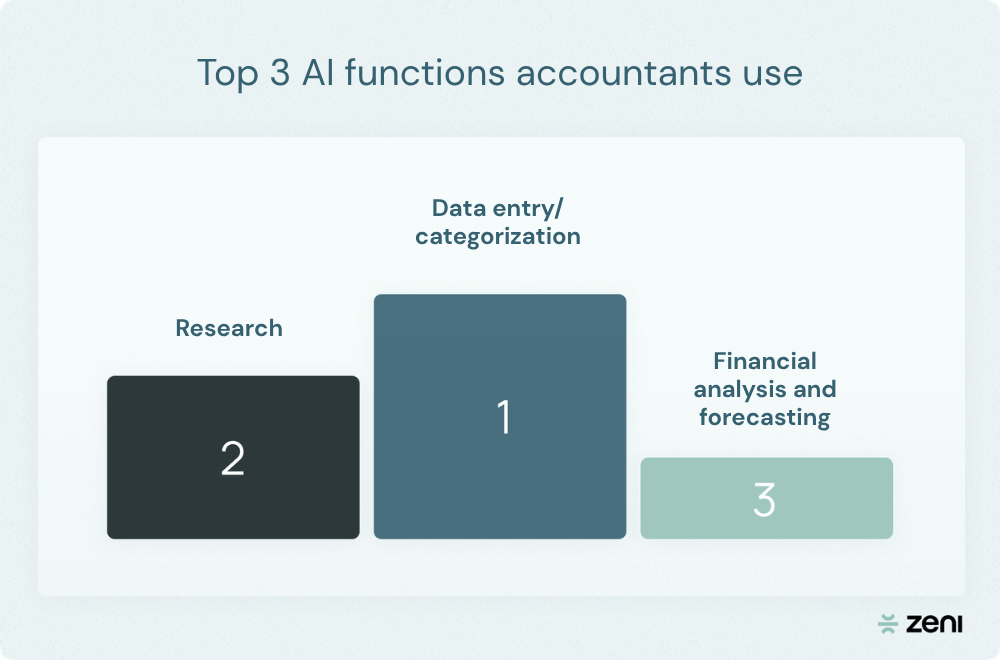

Accountants are using AI across a wide range of accounting workflows, from administrative tasks to higher-level financial analysis. However, the most common use cases tend to be those that involve processing large amounts of information quickly.

Data entry topped the list, with 51% of respondents reporting that they use AI for categorization tasks.

Research (46%), financial data analytics and forecasting (44%), report generation (41%), and bank recs (36%) were the next most common applications.

These tools are producing meaningful time savings for most of our survey respondents, 42% of whom estimated that AI saves them between one and five hours per week, while another 25% said it saves between six and 10 hours.

The impact is even more significant for some users. Nearly one in five respondents (18%) reported saving more than 11 hours per week through AI adoption. Only 15% said AI currently saves them less than one hour per week or no time at all.

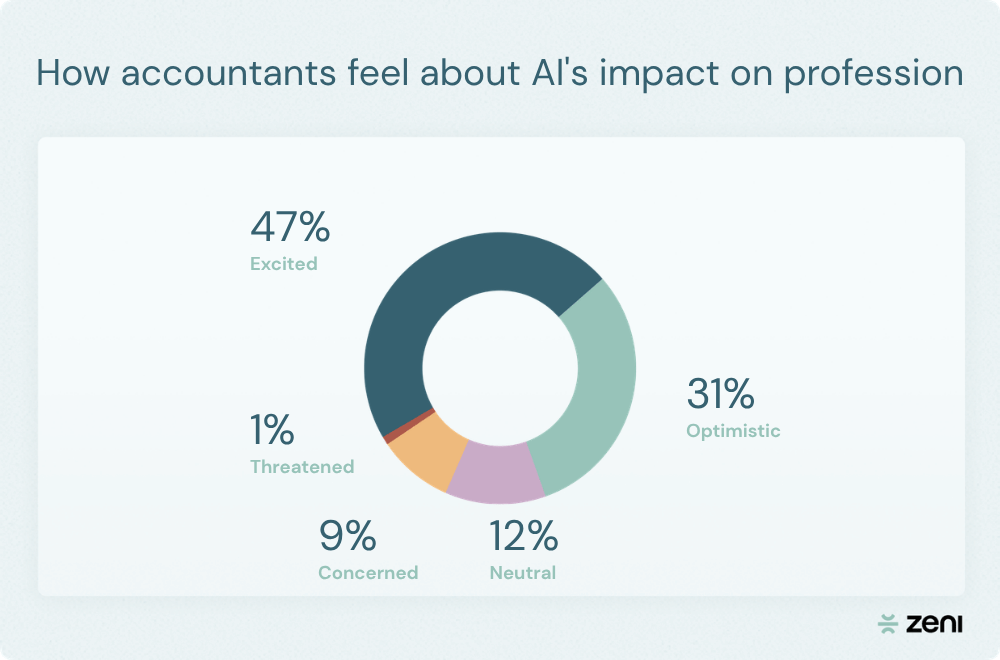

Despite the discourse around AI and job displacement, many accounting professionals have a positive view of AI. Roughly half of our respondents (47%) described themselves as excited about AI's role in the profession, and another 31% said they felt optimistic.

Meanwhile, relatively few respondents expressed negative sentiment. Only 9% said they were concerned about AI, and just 1% described themselves as threatened by it.

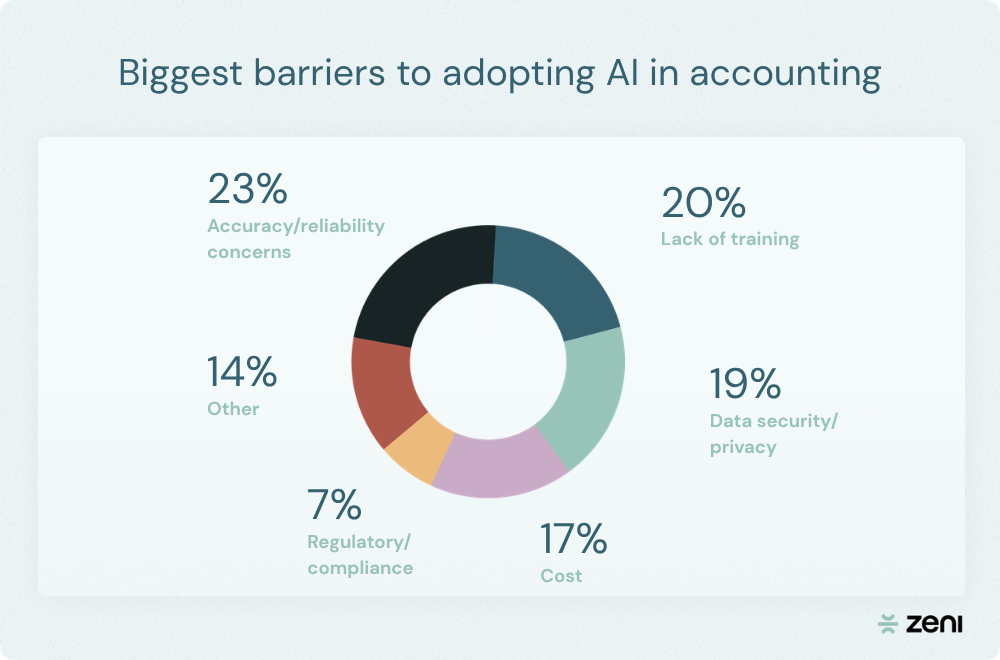

That said, enthusiasm doesn't always translate to easy adoption. Accuracy and reliability concerns were the most commonly reported barrier to AI use (23%).

Lack of training (20%) followed closely behind, which aligns with our other finding that only 61% of accounting employers have provided any AI training.

Accounting firms and finance professionals generally expect AI to play a larger role in their work over the next few years. Half of respondents believe their AI use will increase significantly, while 34% foresee it increasing somewhat.

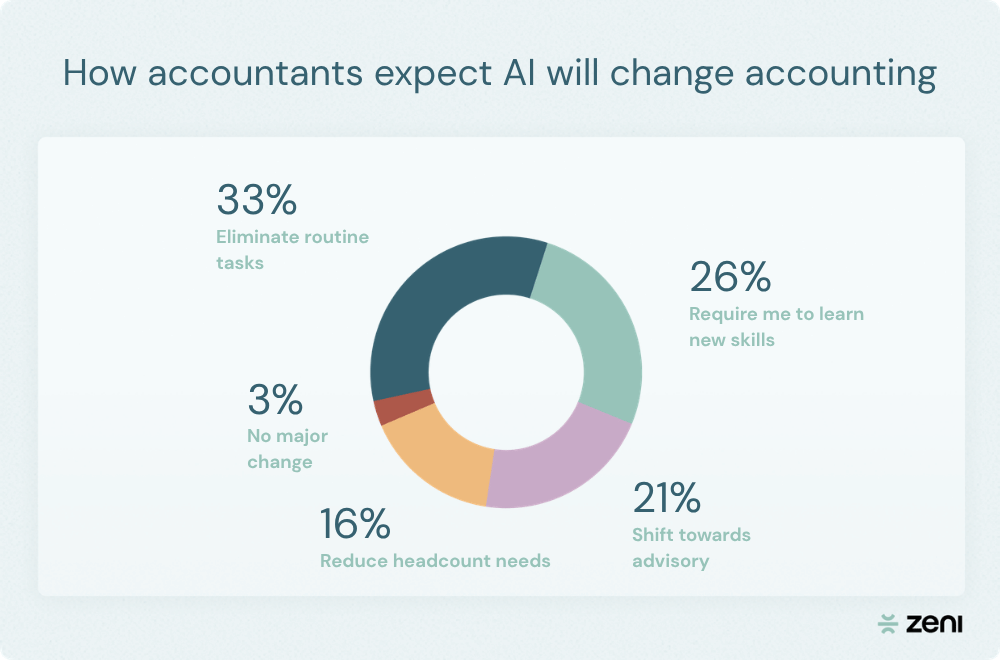

Most respondents view AI primarily as an efficiency driver, with nearly two-thirds (64%) expecting AI to eliminate routine tasks. Another 41% believe their work will shift toward more advisory and strategic services, and 32% expect it to reduce headcount needs.

Many accounting professionals plan to use the extra capacity freed through automation to take on extra clients, including 59% of survey respondents. Another 49% expect to put the additional hours toward strategic planning, and 42% toward reducing burnout.

These expectations are already shaping investment decisions. When asked about their biggest priority for the coming year, 33% of respondents said AI tools, coming in ahead of accounting talent acquisition (24%) and expanding advisory services (19%).

![VC due diligence checklist [downloadable Excel + Sheets]](https://cdn.prod.website-files.com/642b3b2440806566d7573934/6a4ebffb55e7de746ffc7ea8_vc-due-diligence-checklist-feature-image.webp)

.png)

.avif)