Ready to invest in AI?

Schedule time with Zeni's finance pros to learn more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

We tested and compared the leading business credit monitoring platforms to find the best options for small and mid-sized companies.

Monitoring your business credit reporting activity across every major credit bureau— including Experian, Equifax, and Dun & Bradstreet—is essential for protecting your company’s personal information and credit reputation.

Each tool was evaluated for accuracy, reporting frequency, ease of use, and alerts.

Our top pick is FairFigure, thanks to its real-time tracking and detailed credit insights.

Depending on your needs, one of the others on our list might be a better fit.

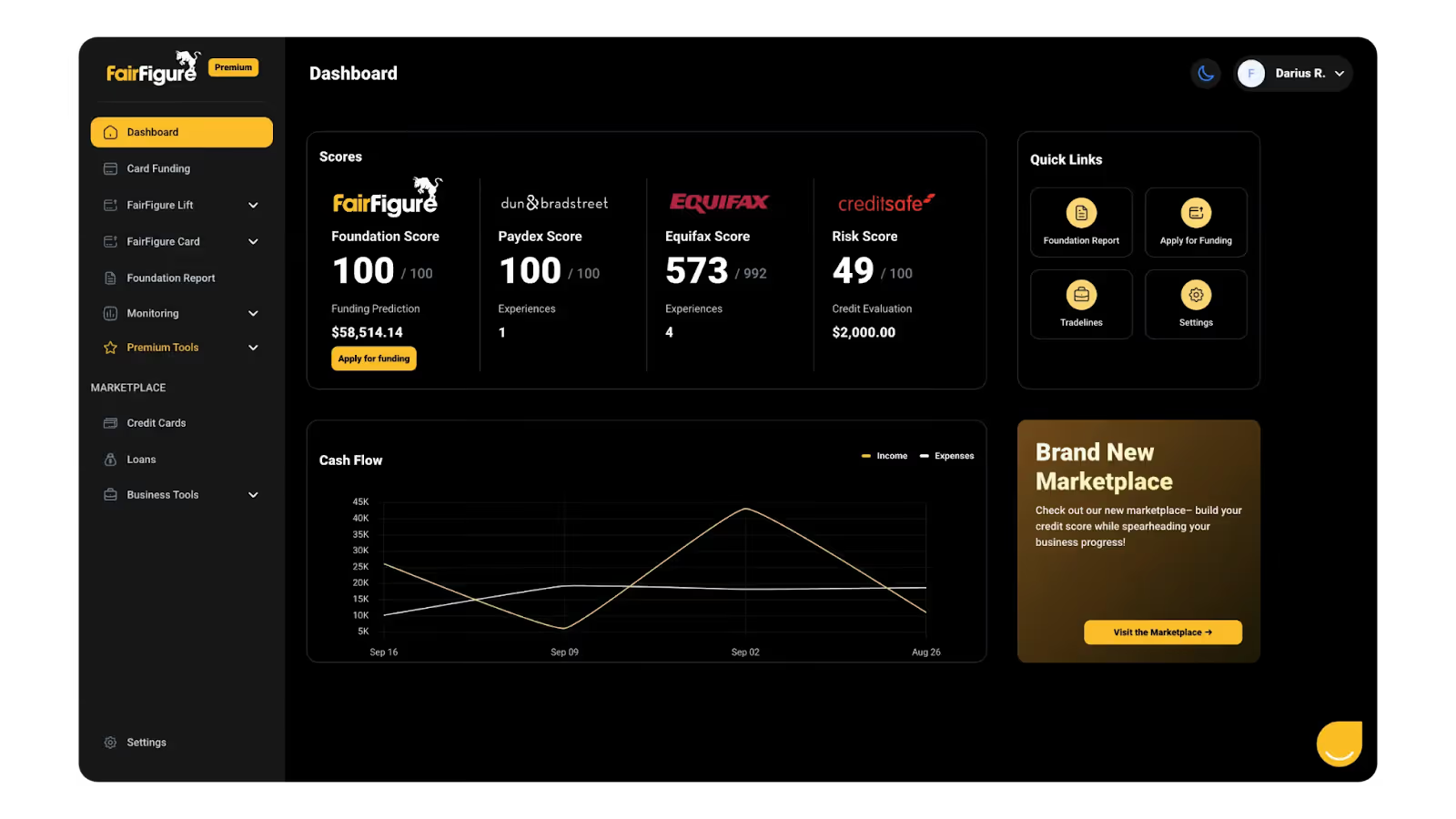

Source: FairFigure

FairFigure positions itself as one of the fastest-growing business credit builder platforms, offering a unique combination of funding, credit monitoring, and credit-building services.

Its tri-bureau monitoring gives you a consolidated view similar to tools like Credit Karma or Credit Sesame, but built specifically for business owners.

It follows a holistic approach to credit building and keeping tabs on your business credit. The FairFigure Card lets you get funded the very same day.

No pesky personal credit checks or guarantees required, as just your EIN is needed, so you can get your hands on capital and start building up that business credit pronto.

Something that both the card and the credit monitoring feature do is report payment history to commercial credit bureaus, giving you potential score boosts.

This kind of reporting helps strengthen both your personal credit score and your business credit account over time.

The good news is that FairFigure takes care of all the credit reporting for you. This just happens to be a great way to get yourself access to better rates, the more your credit improves over time.

The process is designed to be fast and hassle-free.

If you’re a business that’s looking to sort out its business credit while also getting some working capital, then FairFigure has got you covered. It’s a one-stop shop that tackles both short-term funding needs and long-term credit development.

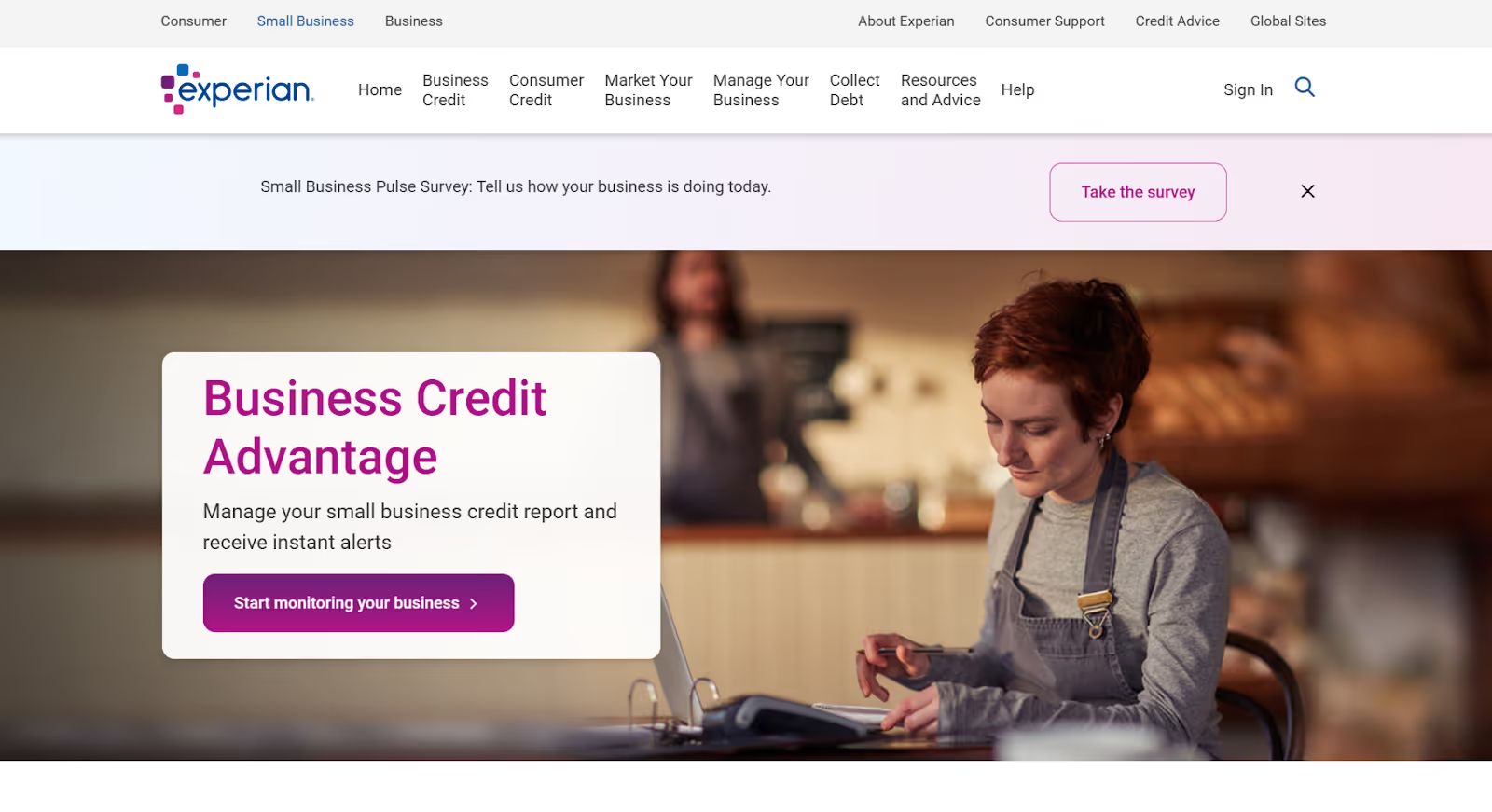

Source: Experian

Experian Business Credit Advantage is a self-monitoring solution for businesses that want to see their Experian business credit profile in detail.

For $199 per year, this annual subscription gives you unlimited, anytime access to your updated Experian credit score and online business credit report.

The monitoring service is proactive as Experian checks business credit daily and tracks changes to your business credit file. It also sends instant email alerts when there are significant changes and inquiries about your business.

Experian’s approach is similar to consumer credit protection platforms but tailored for commercial use, helping safeguard sensitive personal information and business identifiers.

A big plus is the inclusion of CyberAgent business identity monitoring, Experian’s priority monitoring technology that proactively detects stolen business identifiable information and compromised confidential data online.

CyberAgent is designed for international level monitoring, breaking language barriers, and detecting identity theft globally.

At any given time, the technology monitors thousands of websites and millions of data points, and alerts you if your business information is found online in a compromised position.

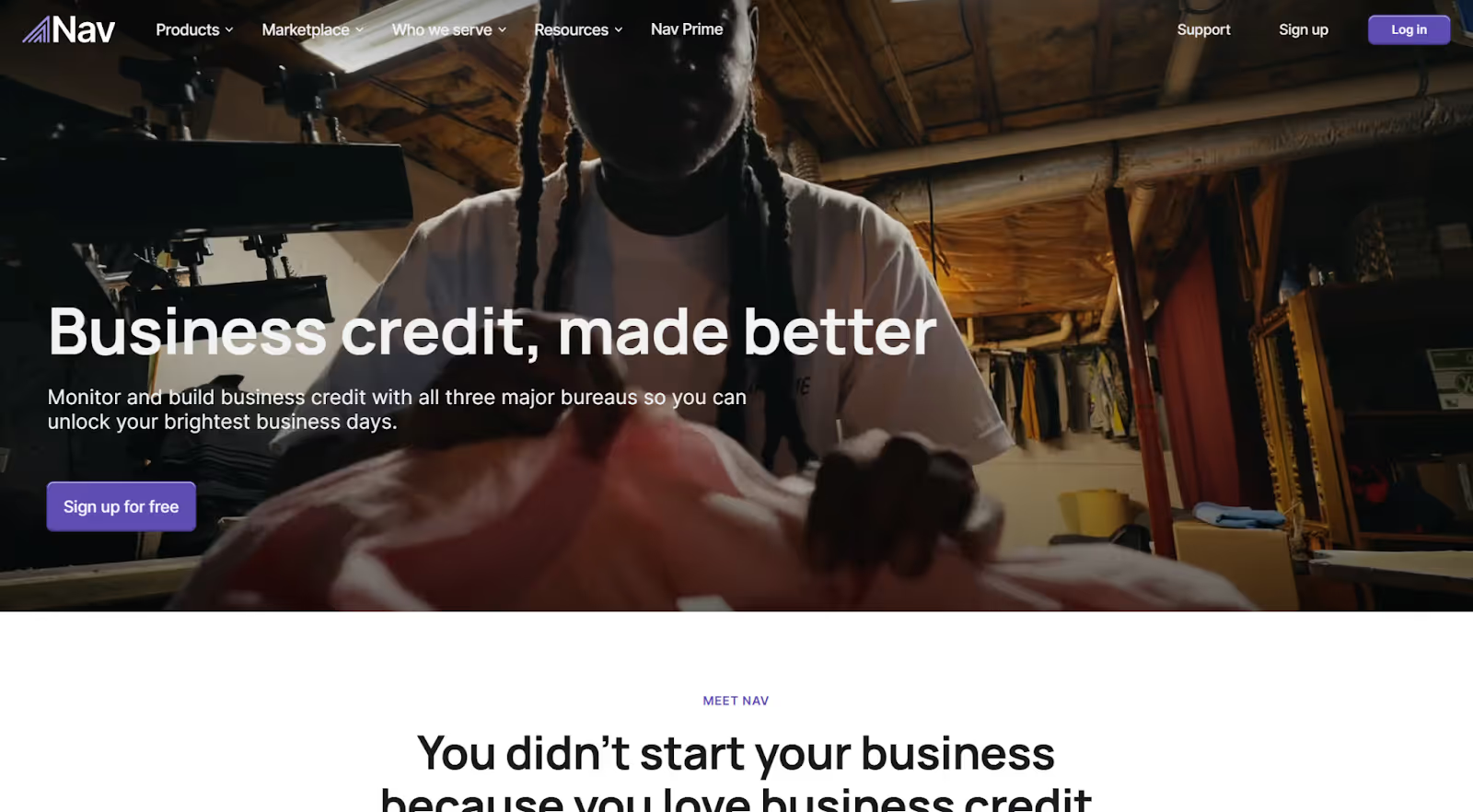

Source: Nav

Nav has made a name for itself as the go to business credit company, with over 2.5 million small businesses across the U.S. who use it.

It acts as an all-in-one credit suite, combining credit repair insights, free credit monitoring, and educational tools to help you build good business credit.

The platform makes users feel like they have a trusted team member by their side, providing guidance on how to navigate the factors that affect business credit.

Nav also has a proven track record of helping businesses see a 40 point average increase across business credit bureaus within the first three months of reporting.

The platform offers a couple of different options:

If you need a bit more from your credit management tool, Nav Prime membership (ranging from $40-$75 per month) has got you covered, offering up to two tradelines as well as features like financing calculators, business checking through Thread Bank (FDIC insured), tax prep, and more.

They also report credit lines to business credit bureaus every month, helping to build good credit habits.

For businesses looking to find out how to build business credit while getting access to a ton of financial tools, Nav lays out your road to success with its combination of guidance, education, and funding opportunities.

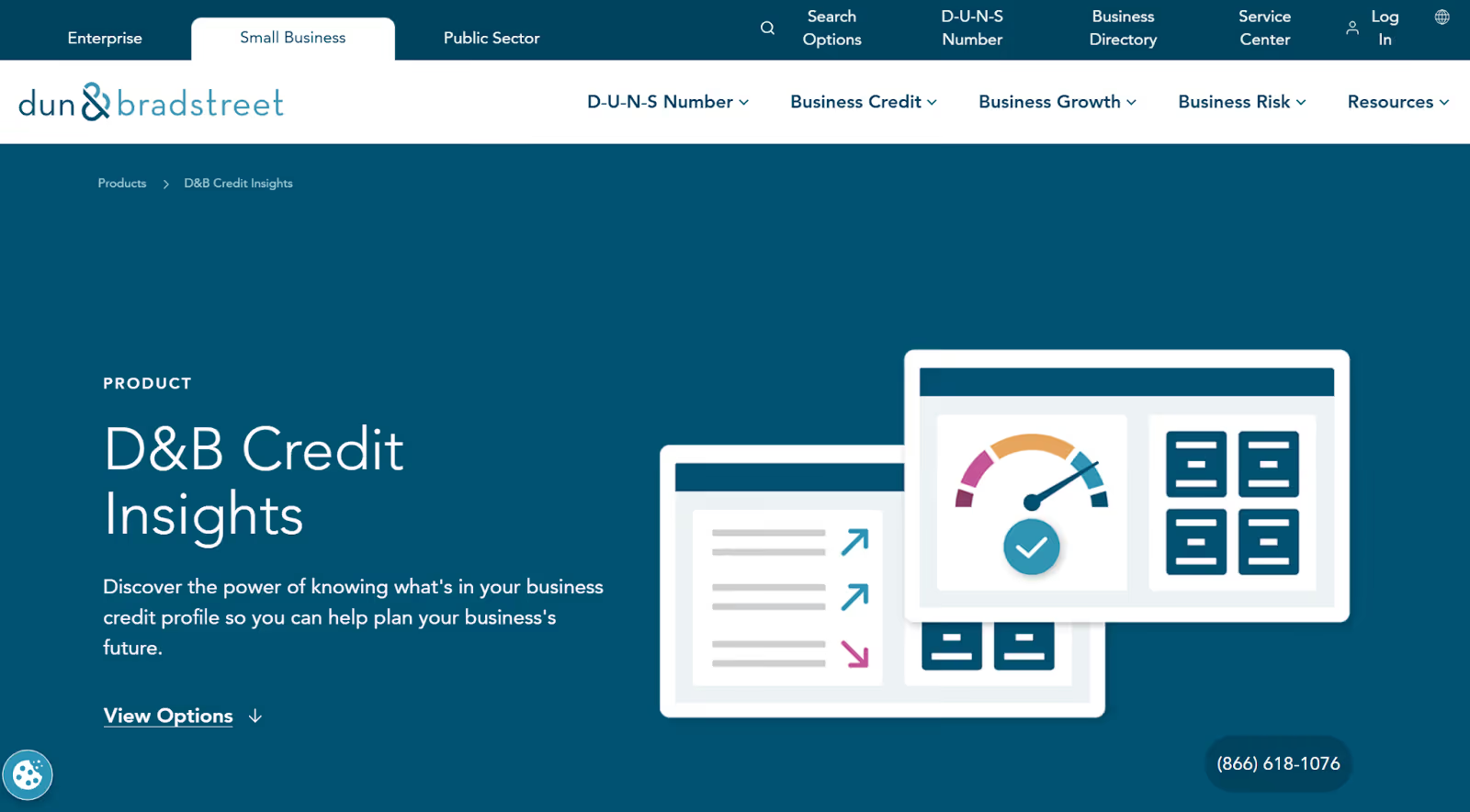

Source: Dun & Bradstreet

D&B Credit Insights is one of the most direct ways to understand and monitor your business credit.

As the oldest and most established bureau, D&B has credit files on millions of businesses, and many major lenders request D&B reports when evaluating business credit applications.

The free Credit Insights tier is for business owners who want to understand their scores and ratings. It provides real-time alerts when there are changes to four key D&B scores: PAYDEX (payment performance), Delinquency Score, Failure Score, and Supplier Evaluation Risk.

These alerts function much like a credit inquiry tracker, helping you see when a credit reporting agency or lender pulls your file.

The free version helps you spot potential issues and act fast, but it also shows directional changes, not actual score numbers, after the initial review period.

Credit Insights Basic ($49/month) is for businesses that need to monitor their credit profile. This tier gives you unlimited access to view your entire D&B credit file, including six D&B scores and ratings with actual numbers visible at all times.

You get real-time alerts when your business credit scores or ratings change, including new inquiries, legal events like lawsuits, liens and judgments, and payment history trends.

Basic also includes dark web monitoring by Flashpoint for up to five business email addresses at no extra cost.

Plus ($149/month) is for businesses that want to build and improve their credit profile. This tier allows you to benchmark your scores and ratings against up to five companies you choose, so you can see how you compare to competitors and set realistic goals.

The platform gives you valuable insights into the business credit scores that matter most to creditors and lenders, so you can make strategic decisions for your business.

Source: Equifax

Equifax Business Credit Monitoring is focused on the small business segment through its massive database and relationships with banks, leasing companies, and suppliers.

Their unique data collection method captures how small business owners manage loan payments, business credit card obligations, and trade credit relationships.

So Equifax reports are particularly valuable for businesses looking for startup credit cards and traditional financing products.

The service keeps a close eye on your business credit file, i.e., your Equifax Business Credit Risk Score (which goes from 101 to 992) and your Equifax Business Failure Score. These metrics are similar to how credit limit utilization affects a personal credit card.

It gives you a pretty good idea of how likely your business is to experience some major payment problems or even go under within the next year (which, in turn, helps you get a handle on how lenders see your credit risk).

Equifax’s service will send you emails if they see any big changes to your Equifax credit report - like new credit checks, changes to your debt-to-income ratio, or a public record update (liens, judgments, or bankruptcies).

There are also alerts on any changes to your payment history with suppliers and creditors.

Equifax isn’t super upfront with their pricing info. You’ll have to get in touch with them for all the details. But they have a huge amount of small business data and some pretty good connections with lenders, so that can be a plus.

It’s perfect if you’re also monitoring credit at other bureaus, especially if your business relies on loans from banks and credit cards, where Equifax data makes a big difference in whether you qualify for a loan.

Source: Creditsafe

Creditsafe is a global business credit and risk management solution with credit information on over 430 million businesses across more than 200 countries.

This makes it the perfect choice for companies that trade internationally, work with international suppliers, or evaluate overseas partners and customers. The platform offers company credit reports, risk scores, and compliance tools through two main products.

For instance, in the UK & Ireland, you can subscribe to a package for registered directors to view your own company’s credit report, get a real-time credit score, view drivers of that score, receive alerts when it changes, and get online support.

You can also get full platform access, which gives you worldwide company credit information and advanced features such as company credit reports, consumer credit & affordability checks, AML/PEP/sanctions screening, global sales/marketing data, integration through APIs, and account management.

Creditsafe uses a scoring system on a 1-100 scale (or 0-100 in some markets) with higher scores signalling lower risk; typically, scores 71-100 are classed “very low risk”. The score is built to predict the likelihood of serious delinquency (90 + days past due) or bankruptcy.

With global identity verification and anti-money laundering checks, Creditsafe is the premium solution for businesses prioritizing international coverage, robust compliance tools, and sophisticated credit management.

Business credit monitoring software is completely different from personal credit monitoring services.

While personal credit reports are private and can only be accessed with your permission under the Fair Credit Reporting Act, business credit reports are public information.

Anyone can see your business credit score and report without your knowledge or consent, this includes lenders, suppliers, landlords, and even competitors.

Business credit scores use different scales, too. Instead of the familiar 300-850 FICO range, business credit bureaus use various scoring systems:

Each bureau weighs factors differently, looking at payment history with vendors and suppliers, credit utilization on business accounts, length of credit history, public records such as liens and judgments, and the size and age of your business.

Business credit monitoring services also track these scores and reports across multiple bureaus, providing:

Choosing the right business credit monitoring service depends on your business needs, budget, and credit goals.

Start by figuring out which credit bureaus matter most to your business:

Consider your budget and how much info you need. Free services like Nav’s basic plan and Dun & Bradstreet are great for businesses new to credit monitoring or cash strapped. These give you enough info to track your scores and get alerts on big changes.

Paid services generally offer more detailed reports, full credit file access, identity protection, and credit building tools that might be worth it if you’re actively looking for financing.

Look at the extra features beyond monitoring. Services that report your subscription payments as tradelines (like FairFigure) give you double value by building credit while monitoring it.

Consider your business stage and growth plans:

Your monitoring strategy should evolve with your business. Start simple and scale up as your credit needs get more complex.

Your business credit score directly impacts every financing decision, vendor relationship, and growth opportunity your company pursues.

Without active monitoring, errors can go undetected for months, fraudulent activity can destroy your credit profile overnight, and you’ll miss opportunities to strategically improve your scores.

The question isn’t one of whether to monitor your business credit, but which service will help you build the strongest financial foundation for sustainable growth.

![VC due diligence checklist [downloadable Excel + Sheets]](https://cdn.prod.website-files.com/642b3b2440806566d7573934/6a4ebffb55e7de746ffc7ea8_vc-due-diligence-checklist-feature-image.avif)

.avif)