Ready to invest in AI?

Schedule time with Zeni's finance pros to learn more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Many business owners want a business credit card without having to connect to their personal credit. That’s where EIN only business credit cards can help.

These cards enable business owners to build business credit, protect their personal credit, and access flexible spending without the need for a personal credit check.

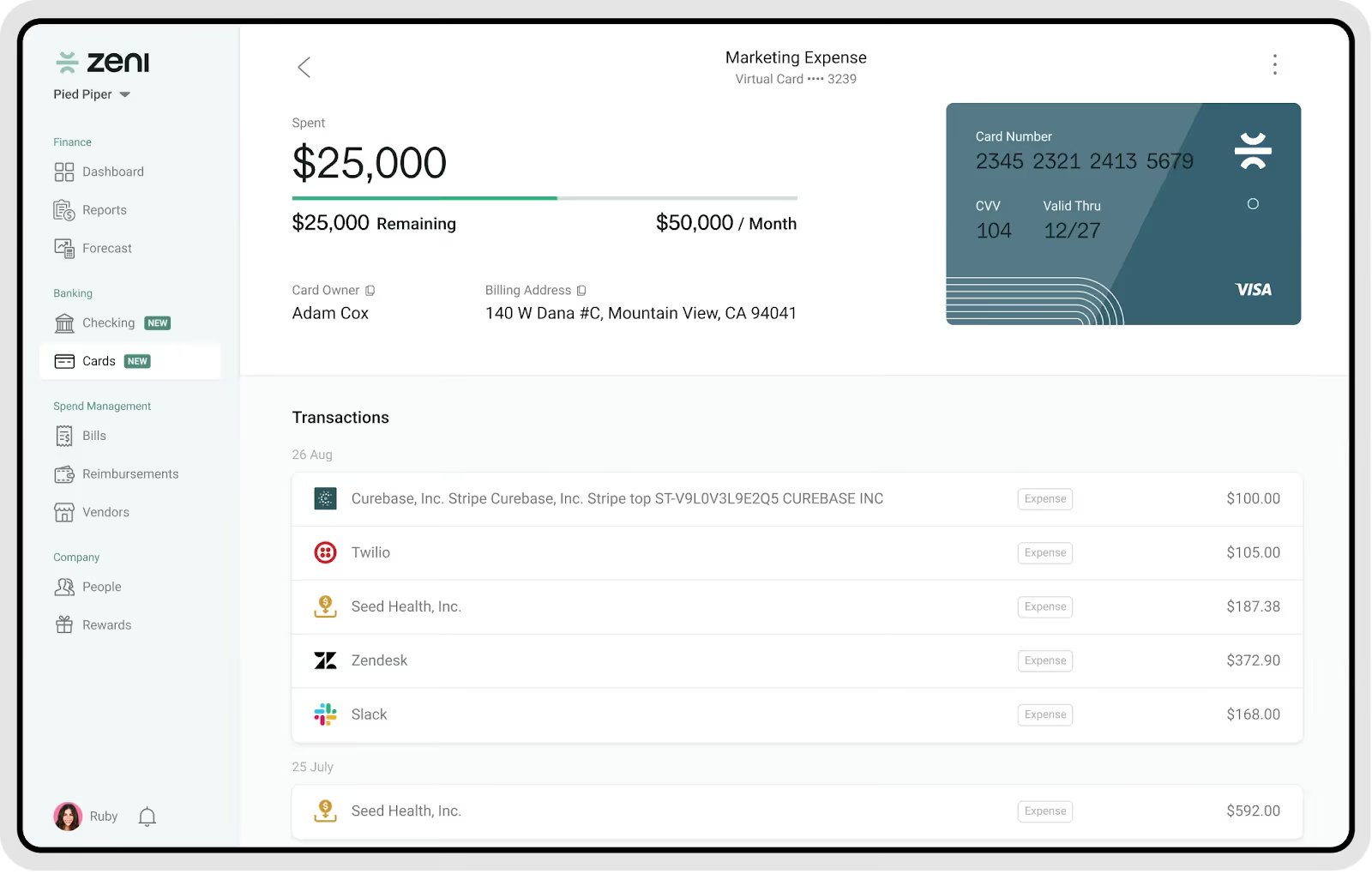

The Zeni Card is the first AI business credit card built for business owners who want speed, accuracy, and real-time visibility across every business card transaction.

It’s part of the Zeni AI-powered ecosystem, which unifies automated bookkeeping, financial management tools, and AI and expert support into a single platform.

Because the Zeni Card integrates directly with Zeni’s AI bookkeeping, every card purchase is automatically categorized. This helps eliminate manual work and ensures every transaction supports timely reconciliation and accurate financial reporting.

The Zeni Card works like a corporate charge card, not like a personal credit card. This protects personal credit and helps companies build business credit based on their financial performance, without mixing personal credit bureaus into the approval process.

It’s also designed for founders who want an EIN only card that aligns spending with real-time cash flow. With AI analyzing transaction data, companies get automatic insights on spending patterns, vendor charges, budgets, credit limits, and more.

The Zeni platform gives businesses:

The Zeni Card also allows teams to issue multiple business cards with precise limits and controls. This helps maintain financial discipline while allowing flexibility for growing teams and distributed employees.

For companies searching for EIN only business credit cards, the Zeni Card offers a unified experience that strengthens financial operations and supports efforts to build business credit. It’s designed to help startups scale smarter with AI and structured corporate credit tools.

The FairFigure Capital Card is a popular choice for business owners who want to build business credit using only their EIN. FairFigure specializes in financial analytics, credit monitoring, and credit-building solutions.

The FairFigure Capital Card is designed to help companies strengthen their business credit history by reporting to each major business credit bureau. For early-stage companies with limited credit history, this makes it a powerful tool to help build long-term financial growth.

This card fits into that ecosystem by giving businesses a simple way to grow their credit profile and monitor their business credit score. It’s especially valuable for small business owners who want to avoid linking a personal credit score or personal credit card to business expenses.

What makes this card appealing is that it helps eliminate the need for a personal credit check. Many business owners want separation between personal and corporate credit, and this card supports that.

As long as businesses maintain on-time payments and responsible usage, they can steadily build business credit.

Key benefits include:

The FairFigure Capital Card is often recommended for entrepreneurs interested in EIN only business credit cards because of its straightforward approach to credit building and financial transparency.

For companies that want a structured business card with predictable terms, this option delivers clarity around credit limits, spending, and card membership requirements. You can learn more about the FairFigure Capital Card directly on their website.

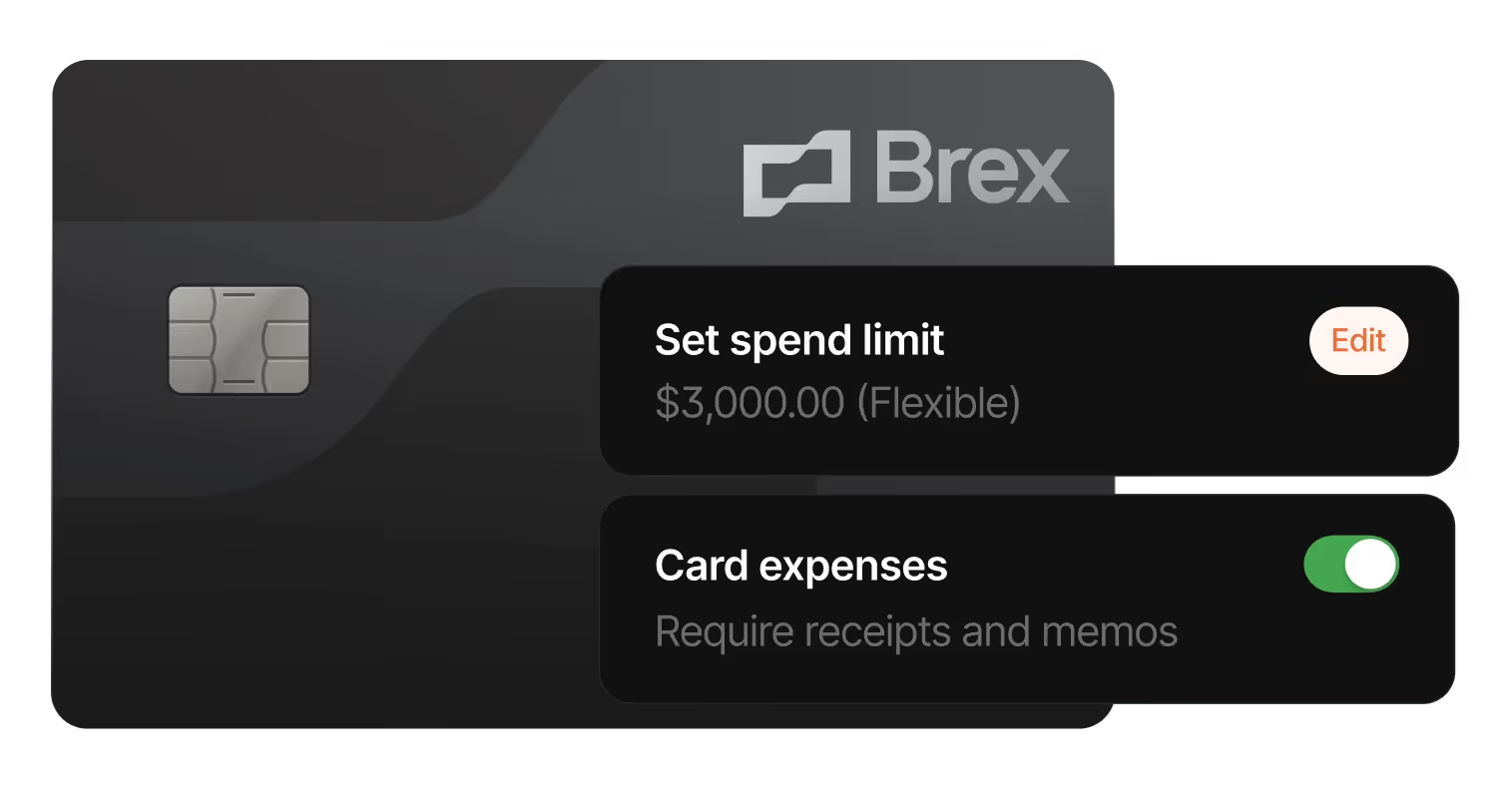

The Brex Corporate Card is widely known for offering high credit limits, fast approvals, and a modern charge card structure.

It’s designed for growing startups that want to avoid using personal credit and instead rely upon a corporate credit evaluation based on revenue, cash flow, and financial activity.

Business owners exploring EIN only business credit cards often consider the Brex Corporate Card because it doesn’t require a personal credit check or personal credit score.

Brex evaluates the health of the business instead, which protects personal credit history and separates business expenses from personal credit bureaus.

The Brex Corporate Card includes:

The Brex Corporate Card integrates with accounting systems and financial tools, making it useful for small business teams with complex spending needs. It provides dynamic credit limits that adjust as the company grows.

Brex also reports to credit bureaus that track corporate credit, helping businesses build business credit over time. This is important for early-stage companies that might need to get a business loan or seek a higher credit limit.

Because Brex focuses heavily on automation, it pairs well with companies already using digital finance tools. It’s one of the strongest alternatives for business owners comparing corporate cards, startup credit cards, or options that don’t require personal credit.

Overall, the Brex Corporate Card remains one of the leading choices for businesses wanting flexible spending power without relying on personal credit.

The Ramp Corporate Card is a charge card designed to help companies spend less, operate more efficiently, and automate financial workflows. It’s especially popular among businesses that want strong cost controls and a card issuer that focuses on savings and efficiency.

Because Ramp evaluates companies based on financial health instead of personal credit history, it’s often listed among the top EIN only business credit cards.

Ramp avoids personal credit checks and personal credit bureaus, helping business owners protect their personal credit while strengthening their corporate credit profile.

Ramp’s platform stands out for its automation features. It identifies duplicate software subscriptions, unused tools, and opportunities to reduce vendor costs. This makes it different from traditional business credit card companies that issue a card without analyzing spending.

The Ramp Corporate Card includes:

These tools support companies trying to build business credit in a structured way. As Ramp reports activity to relevant credit bureaus, it helps establish a solid business credit score over time.

Many small business teams choose Ramp because it simplifies compliance, improves budget management, and reduces manual processes. That makes it an attractive choice for business owners who want a corporate card that adds operational value, not just a payment method.

Ramp also appeals to companies that want predictable terms from a credit card without interest charges or hidden fees. For startups with fast-growing expenses, it’s a strong alternative to traditional business card options.

The Stripe Corporate Card is built specifically for internet-first businesses, e-commerce brands, and SaaS startups. It evaluates businesses differently from a traditional credit card issuer. Instead of relying on personal credit history, Stripe reviews revenue and Stripe payment volume.

This process makes the Stripe Corporate Card one of the top EIN only credit card options, especially for digital businesses.

Stripe avoids personal credit checks and focuses heavily on business performance, protecting the founder’s personal credit score and personal credit history.

Businesses benefit from:

The Stripe Corporate Card reports to business credit bureaus, helping companies build business credit and improve their business credit score. For small business teams with limited credit history, this is a valuable advantage.

Because the corporate card ties directly into Stripe’s payment infrastructure, companies gain seamless visibility into spending and financial activity. This is useful for founders who want real-time clarity into credit limits and card usage across teams.

The card's structure makes it ideal for companies that already rely on Stripe for payment processing. It becomes an extension of existing financial operations, especially for e-commerce brands that want higher credit limit flexibility without relying on a personal credit card.

For companies comparing corporate cards and EIN only business credit cards, the Stripe Corporate Card remains one of the most popular choices for online-first businesses and high-growth startups.

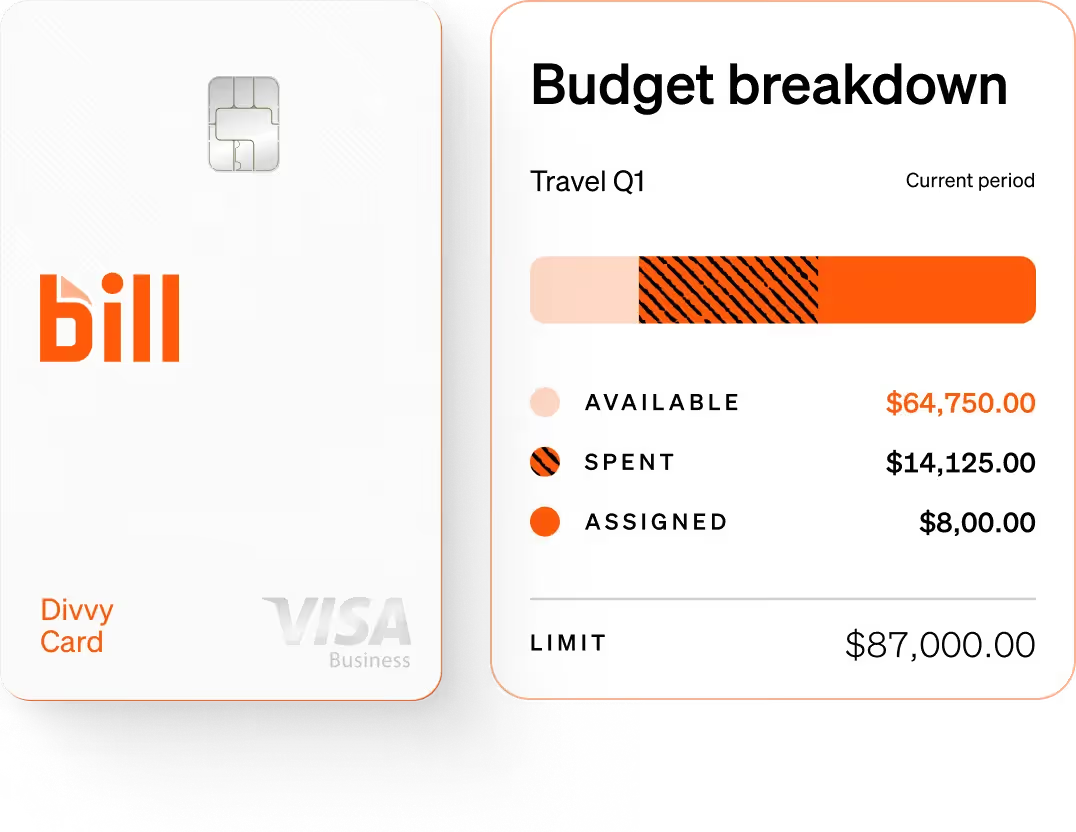

The BILL Divvy Card (previously known simply as the Divvy Card) is built for businesses that want budgeting and expense management connected to their corporate card.

It operates as a charge card, which means companies must pay in full each cycle, helping them avoid interest charges while maintaining structured spending.

The BILL Divvy Card does not rely heavily on personal credit. It analyzes business cash flow, balances, and financial stability instead. Because it avoids personal credit checks, business owners researching EIN only business credit cards frequently consider Divvy as an option.

Divvy combines card tools with detailed budgeting features. Each business card can be assigned a unique spending limit, category, and approval workflow. This helps to reduce overspending and can keep finance teams in control.

Key BILL Divvy Card features include:

Activity for the BILL Divvy Card is reported to business credit bureaus, helping companies build business credit and strengthen their business credit history. This is valuable for businesses planning to apply for a business loan, a higher credit limit, or secured business credit cards.

Because the BILL Divvy Card links every transaction to a specific budget, it’s ideal for teams with distributed spending or multiple departments. It gives companies transparency while protecting personal credit and keeping business expenses fully separate.

For businesses comparing corporate cards or startup credit cards, the BILL Divvy Card offers a balanced approach that simplifies budgeting and strengthens financial discipline.

Applying for an EIN only credit card is simpler than many business owners expect. The process depends on the credit card company, but most EIN only business credit cards follow similar requirements.

Start by confirming that the business credit card supports EIN-only applications. Many corporate credit cards, such as Brex, Ramp, and the Stripe Corporate Card, avoid personal credit checks entirely. This helps create a clean separation between personal and corporate credit.

Next, gather the business documentation. Most credit card companies require:

Some card issuers may also review the business credit history, though this is not always required for new businesses.

Once approved for the best business credit card, businesses should use the card responsibly to build business credit. Paying on time, maintaining healthy credit limits, and monitoring credit bureau reporting help strengthen business credit scores over time.

For a full overview, visit Zeni’s guide on how to build business credit. For comparisons of card options, view Zeni’s articles on business credit cards and startup credit cards.

Most EIN only business credit cards share similar requirements. Unlike personal credit cards, these products evaluate business performance instead of personal credit bureaus or personal credit history.

You’ll generally need:

Some corporate card issuers focus on financial activity and revenue rather than business credit history. Others may require a minimum balance in your bank account or a minimum business duration.

Companies with established business credit scores may receive better credit limits, easier approvals, and more favorable terms. Newer companies can still qualify for many EIN only cards because approval is often based on cash flow, not years of credit history.

Business owners choose EIN-only cards to avoid personal credit checks and maintain a clear separation between corporate credit and personal credit. This helps protect the small business owner while enabling the company to build business credit and strengthen its financial position.

Platforms like Zeni make it easier to manage transactions, maintain accurate reporting, and keep financials clean. These are important factors when applying for EIN-only cards that rely on real-time financial performance.

EIN only business credit cards help business owners protect personal credit while building strong business credit.

Whether you choose the Zeni Card or compare other corporate cards, selecting the right option can improve financial visibility, simplify operations, and support long-term growth for your small business.

.png)

.png)

.png)

.avif)