.avif)

Ready to invest in AI?

Schedule time with Zeni's finance pros to learn more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Determining whether you owe the alternative minimum tax (AMT) is enough to give anyone a headache. It requires you to calculate your taxes twice—once using the regular rules, then again under a completely separate system.

This guide walks you through the process step by step, including a detailed example. We’ll also explore AMT tax planning strategies and highlight some of the most significant variables involved.

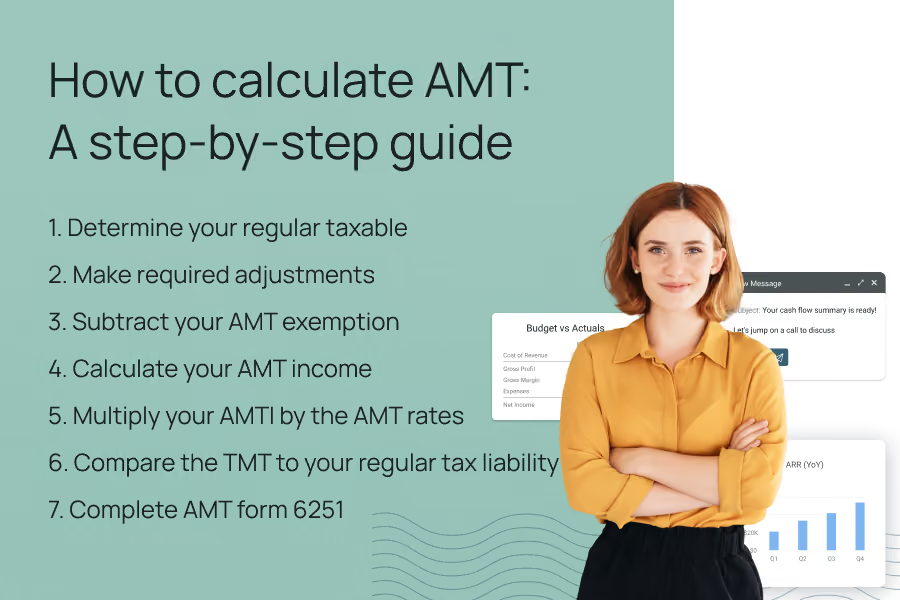

Calculating the AMT requires a series of steps that go a bit further than your regular tax calculation. Each step involves specific calculations to determine your AMT liability and what adjustments need to be made. Below is a detailed breakdown of these steps.

1. Determine your regular taxable income

Your first step is to calculate your household income per the regular tax rules, which is your gross income minus any deductions (either the standard deduction or itemized deductions), exemptions, and credits on your regular tax return.

You can use a regular tax calculator to help you determine the amount, which serves as the baseline for your AMT calculations.

2. Make required adjustments

Next, make the required AMT adjustments to your taxable income. These adjustments include adding back certain itemized deductions from Schedule A, like state and local taxes (SALT), certain mortgage interest tax deductions, and differences in allowable depreciation amounts.

You also have to add back the standard deduction if you claimed it instead of itemizing, which is only deductible for regular tax purposes. For an exhaustive list of each AMT adjustment, refer to IRS Form 6251.

3. Subtract your AMT exemption

Depending on your income threshold, subtract the AMT exemption dollar amount from your adjusted gross income. The exemption decreases for high-income earners at certain thresholds.

Make sure to double-check that you're using the correct exemption amount, as it varies significantly between filing statuses and gets updated regularly for inflation.

4. Calculate your AMT income

After subtracting the AMT exemption amount, the result is your alternative minimum taxable income (AMTI). This amount will be used to compute the tentative minimum tax (TMT).

5. Multiply your AMTI by the AMT rates

Once you have your AMTI, you'll apply the AMT rates to it. For the tax year 2025, the AMT rates are 26% and 28%. The rate depends on the level of your AMTI.

For example, for a single filer, the 26% rate is applied to AMTI up to $239,100, and the 28% rate is applied to any AMTI above that threshold. For married couples filing separately, the 26% rate applies to AMTI up to $119,550, and the 28% rate applies to AMTI above that threshold.

6. Compare the TMT to your regular tax liability

Your tentative minimum tax is compared to your regular tax liability. If your TMT is higher, the difference between the TMT and your regular tax liability is the AMT amount that you owe.

7. Complete AMT form 6251

Finally, fill out the alternative minimum tax form 6251 to formally calculate and report your AMT. This form reflects AMT adjustments, taxable income, AMT exemption, and AMT credit, if applicable, to arrive at your tax liability.

By following these steps precisely, you can accurately determine whether you're subject to the alternative minimum tax and, if so, how much you owe. An AMT calculator may help streamline the process.

It's also worth noting that for those abroad, the foreign tax credit may be able to offset a portion of the AMT owed. If you're unsure about your eligibility for this credit, consult with a tax professional.

Say you’re a single filer who took itemized deductions for 2025 and you want to check if you owe AMT for the year. After reviewing your Form 1040, you know the following facts:

First, you add back the AMT adjustments to your regular taxable income to calculate your AMTI:

AMTI = $70,000 + $10,000 + $3,000 + $5,000 = $90,000

Next, you subtract your AMT exemption from your AMTI to calculate your AMT income:

AMT Income = $90,000 – $88,100 = $1,900

With that, you can multiply your income by the applicable AMT rate to get your TMT:

TMT = $1,900 x 26% = $494

Finally, you can compare the $494 AMT to your regular tax of $10,314 and determine that the regular tax is higher. As a result, you aren’t subject to AMT for 2025.

Tax planning is rarely straightforward, but tax planning for the AMT can be especially complex. AMT tax triggers are largely unrelated, making it difficult to address them all with a single strategy.

In addition, taking steps to avoid AMT often affects your regular taxes. If you’re not careful, you can cause them to increase as much or more than you would save by avoiding the AMT.

In many cases, AMT planning involves forecasting your tax liabilities several years in the future. If you expect to owe AMT in one year and not the next, you can accelerate or defer income to the year with the lowest marginal rate to find savings.

This is easiest when you have some control over the timing of your earnings, such as a Schedule C business owner who can decide when to invoice clients. However, you can also accomplish it by making contributions to certain tax-advantaged accounts.

Fortunately, any AMT you pay due to temporary differences between regular and AMT deductions—like depreciation timing differences—creates a minimum tax credit (MTC) you can use to offset regular taxes in future years.

Beyond this, more advanced strategies often involve making specific elections in regard to how you’re claiming deductions like depreciation under the regular tax system. Ideally, this can reduce or eliminate the associated AMT adjustment, but it’s a delicate process.

When in doubt, it’s a good idea to work with a Certified Public Accountant (CPA) who can help you model out your AMT liability and determine the most efficient way to minimize it.

AMT and ISOs

Incentive stock options (ISO) are a form of equity compensation that allows employees to purchase the company’s shares at a fixed exercise price.

Under the regular tax system, exercising an ISO isn’t a taxable event. You only have to worry about owing capital gains taxes when you eventually sell your shares.

However, the AMT system treats the difference between your exercise price and the fair market value (FMV) of the underlying shares on the exercise date—called the bargain element—as taxable income.

Bargain Element = FMV at Exercise – Exercise Price

For example, say you have an ISO with an exercise price of $10. When your company’s stock is worth $25 per share, you exercise the option.

Under the regular tax system, this is a non-taxable event. But under the AMT system, it generates income equal to the bargain element.

Bargain Element = $25 – $10 = $15

At scale, this can generate a significant amount of AMT income, even though you haven’t completed a sale or received any cash.

As a result, employees should always have a tax strategy in place before exercising ISOs to avoid having to pay AMT. For example, one common approach is to exercise ISOs gradually over multiple years.

Alternatively, you might exercise early in the year, giving yourself time to sell before year-end if your expected AMT bill gets too high. This would make the sale a “disqualifying disposition,” eliminating the bargain element from your AMT income—but at the cost of your gains being short-term gains under the regular tax system.

Maintain your tax compliance

Whether you're learning how to write off business expenses or searching for unique tax breaks to lower your startup's taxes, maintaining compliance is crucial for avoiding penalties and potential legal consequences.

As your business grows and changes, so too will your tax responsibilities. A key part of this is understanding and correctly calculating the alternative minimum tax.

By following the steps outlined above, you can avoid any surprises come tax time and stay in good standing with the Internal Revenue Service.

Make sure to revisit the AMT calculation process each tax season for informational purposes, such as making changes to your filing status or tax laws. Remember, the AMT rules are complex, and you may require the assistance of a qualified tax professional to ensure accurate reporting.

By staying informed about both your personal and your startup's annual tax obligations, you'll be able to spend more time and energy on what really matters — your business.