.avif)

.avif)

The ultimate finance cheat sheet

Search for answers or explore resources to navigate every financial decision.

Please wait for items to load

.webp)

.avif)

.avif)

.png)

Guides

May 5, 2025

All

Tariffs are hitting everything—Even your business funding

Guides

November 19, 2024

All

Foreign Reporting

Guides

November 12, 2024

All

2025 Business Tax Deadlines

Guides

July 9, 2024

All

Payroll Year-End Reminder Checklist

Guides

March 25, 2024

All

Understanding Updates To Section 174

Guides

February 22, 2024

All

Understanding Your Eligibility for R&D Tax Credit

Guides

August 21, 2023

All

.webp)

Zero-Based Budgeting: Maximize Returns On Every Investment

Guides

June 29, 2023

All

Maximizing Your Startup Runway: Tips for Long-Term Growth

Guides

May 30, 2023

All

.avif)

The Future Of Financial Operations: Startup Finance Reimagined

Guides

April 28, 2023

All

How To Leverage The Role Of The Fractional CFO

Guides

April 29, 2023

All

Mastering CFO And Investor Relations: A Step-By-Step Guide

Guides

April 29, 2023

All

A How-To Guide On Building Financial Models

.avif)

.avif)

Case Studies

All

July 22, 2026

.png)

How Alliance Golf Got 30+ Hours a Week Back to Focus on Growth

Case Studies

All

June 29, 2026

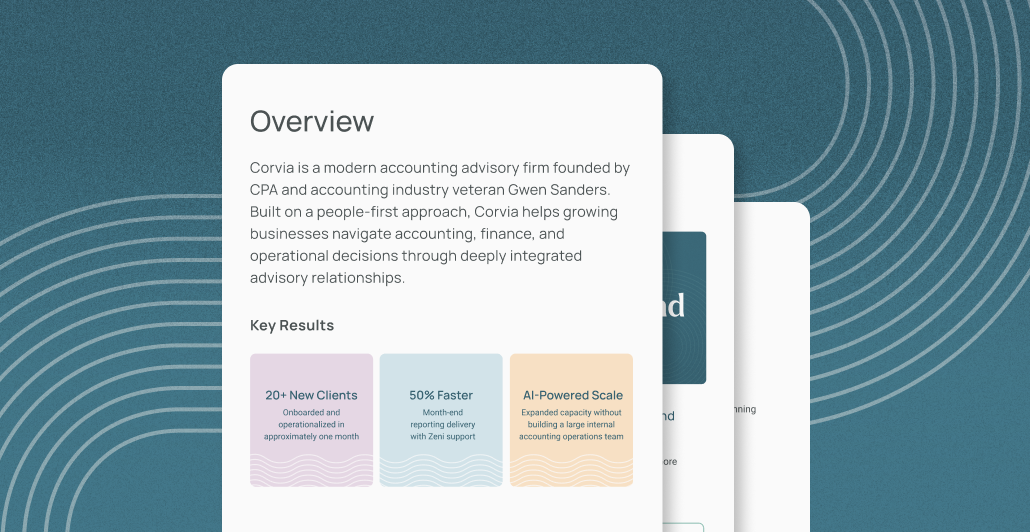

How Accounting Firm, Corvia Scaled Its Advisory-First Accounting Model with Zeni

Case Studies

All

May 19, 2026

.avif)

How Blackleaf Used Zeni’s AI-Powered Finance Platform to Scale a Premium Vodka Brand with Confidence

Case Studies

All

December 8, 2025

.avif)

Scaling Financial Operations with Zeni's Fractional CFO Services

Case Studies

All

January 24, 2025

.avif)

How Wander Maps was able to collect $60,000 in R&D tax credit using Zeni

Case Studies

All

October 23, 2023

.webp)

How An All-In-One Financial Platform Saved TeamBridge 53 Hours Per Month

Case Studies

All

August 29, 2023

.avif)

Campfire Raised $1.25 Million With The Help Of Zeni’s Real-Time Accounting And Investor Reporting

Case Studies

All

July 14, 2023

.webp)

How Real-Time OpEx Reports Helped Matic Make Decisions 10x Faster

Case Studies

All

June 26, 2023

.webp)

How GAAP-Compliant Financial Reports Helped Caravel Labs

Case Studies

All

April 27, 2023

How A Winning Financial Model Helped RegScale Raise A $20M Series A

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.