.avif)

.avif)

Ready to invest in AI?

Schedule time with Zeni's finance pros to learn more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

The best banks for startups offer significant benefits over most traditional institutions, including superior interest rates on deposits, much higher FDIC insurance coverage limits, and little to no recurring fees or minimum opening deposit requirements.

Here are our top five recommendations for accounts that meet these criteria and everything you need to know about their pros and cons to determine which of them is the right bank for you.

Zeni is an AI bookkeeping software backed by a dedicated finance team. One of their products includes Business Checking Accounts.

Mercury is a tech-focused bank built for startups. While it specializes in working with tech companies, any type of business can bank with Mercury.

One of the biggest benefits of Mercury is its incredibly straightforward offering and easy-to-use platform. For example, startups can sign up and gain access to a business checking and savings account and a debit card in as little as 15 minutes.

See also: 8 Best Accounting Tools for Startups

While Brex Cash technically isn’t a bank, we decided to include it here for their “cash management account” offering. A cash management account (CMA) provides all that a business bank account does with fewer fees. You can manage all transactions on one portal, make deposits, trade securities, and even write checks with a CMA.

In 2021, Brex Cash raised a whopping $425 million through its Series D round to help it create a more comprehensive financial solution for startups and businesses.

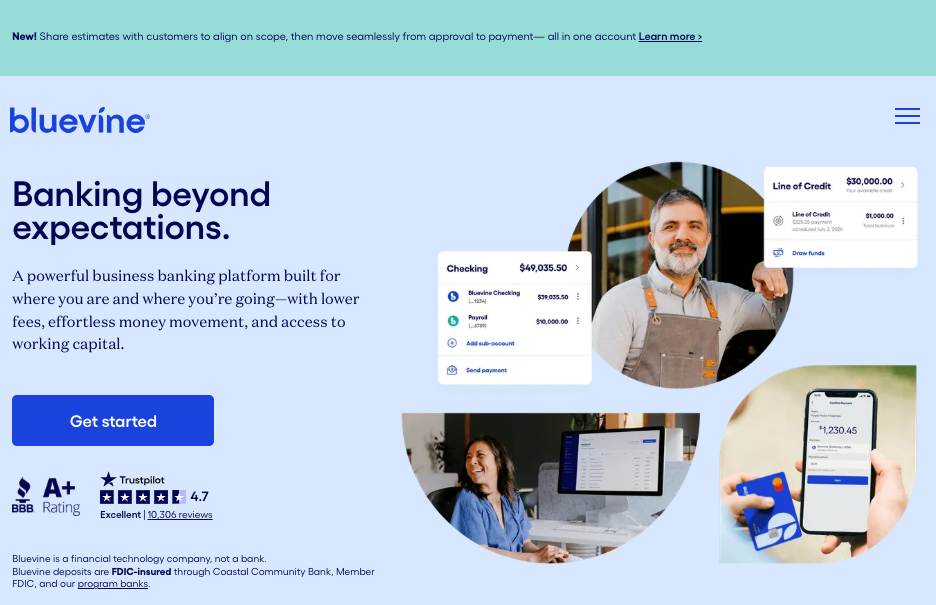

Bluevine is a digital banking platform designed specifically for self-employed individuals, small businesses, and startups.

It uses a tiered subscription model, with the Standard plan providing free access to its essential banking tools. These include high-yield interest earnings, integrated bill pay, and flexible payment acceptance.

You can also upgrade to a paid plan for $30 or $95 per month to get increasingly advanced features and cheaper transaction fees, such as lower incoming and outgoing international wire costs.

Regardless of your subscription tier, Bluevine Business Checking Account users gain streamlined access to the platform’s business line of credit.

Wells Fargo is one of the most well-known banking solutions for individuals and businesses and is a leading small business bank. Even as a well-established financial institution, they offer many perks for startups, including an excellent small business credit card and small business loans.

They also offer different business checking accounts; for startups, the Navigate Business Checking Account includes up to 250 transactions and $20,000 in cash deposits processed per fee period at no charge. This type of account supports new and growing businesses with a steady volume of banking activity.

See also: Startup Bookkeeping: Common Mistakes VC-Backed Startups Make and How We're Solving Them

Other options for startup banking accounts range from simple checking and savings accounts, to more complex money market accounts and cash management accounts.

Before moving forward with the application process, be sure you and your business meet the qualifications to open a business bank account.

New entries into the startup banking industry offer the most competitive low and no-fee banking products and services.

Details of each bank’s fees are available via their respective landing pages, where you can sift through the fine print:

Startup founders are on the go 24/7 and require a banking partner who can rise to the occasion to meet their needs. This chart will help you judge how easy it will be to access your company’s bank account or contact customer support about an urgent matter.

See also: Accounting Software Comparison for Startups

Account security is paramount when deciding where to store your startup’s cash.

See also: Startup Bookkeeping: Common Mistakes VC-Backed Startups Make and How We're Solving Them

Whether you're evaluating a banking partner for a new business or looking to change your current banking setup, use this guide to help you compare the top startup banking options, including business checking accounts, for your needs.

While finding the bank with the best business banking features is crucial, your financial management efforts will benefit tremendously from expert assistance. For the rest of your startup's finance-related needs, take a closer look at Zeni.

Zeni uses a combination of AI and human finance experts to maintain accurate books and manage all of your financial functions. Services include daily bookkeeping, ongoing accounting services, access to our finance concierge, bill pay and invoicing, budgeting and projections, annual taxes, CFO services, and streamlined management of your business checking account.

Zeni customers also gain access to a single dashboard to view and manage their finances in real-time, including their business checking account activity.

Manage your cash flow effortlessly with Zeni. Book a free demo to learn about our real-time bookkeeping and comprehensive financial management so you're always in the loop with your finances.

.png)

.png)

.png)