Ready to invest in AI?

Schedule time with Zeni's finance pros to learn more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

When we think of business transactions, the majority of us probably think of utilizing cash, credit, or debit cards. Most big businesses accept major credit cards and pay hefty processing fees without a problem. But for startups that might have small budgets or are more carefully managing their cash flow, these fees can pile up.

On average, credit cards charge between 1.5% - 3% for each transaction. ACH payments offer small businesses and startups a near instant payment type that works quicker than other forms of payment.

This blog post will explore the different options and help you find the best ACH payment processors for your business.

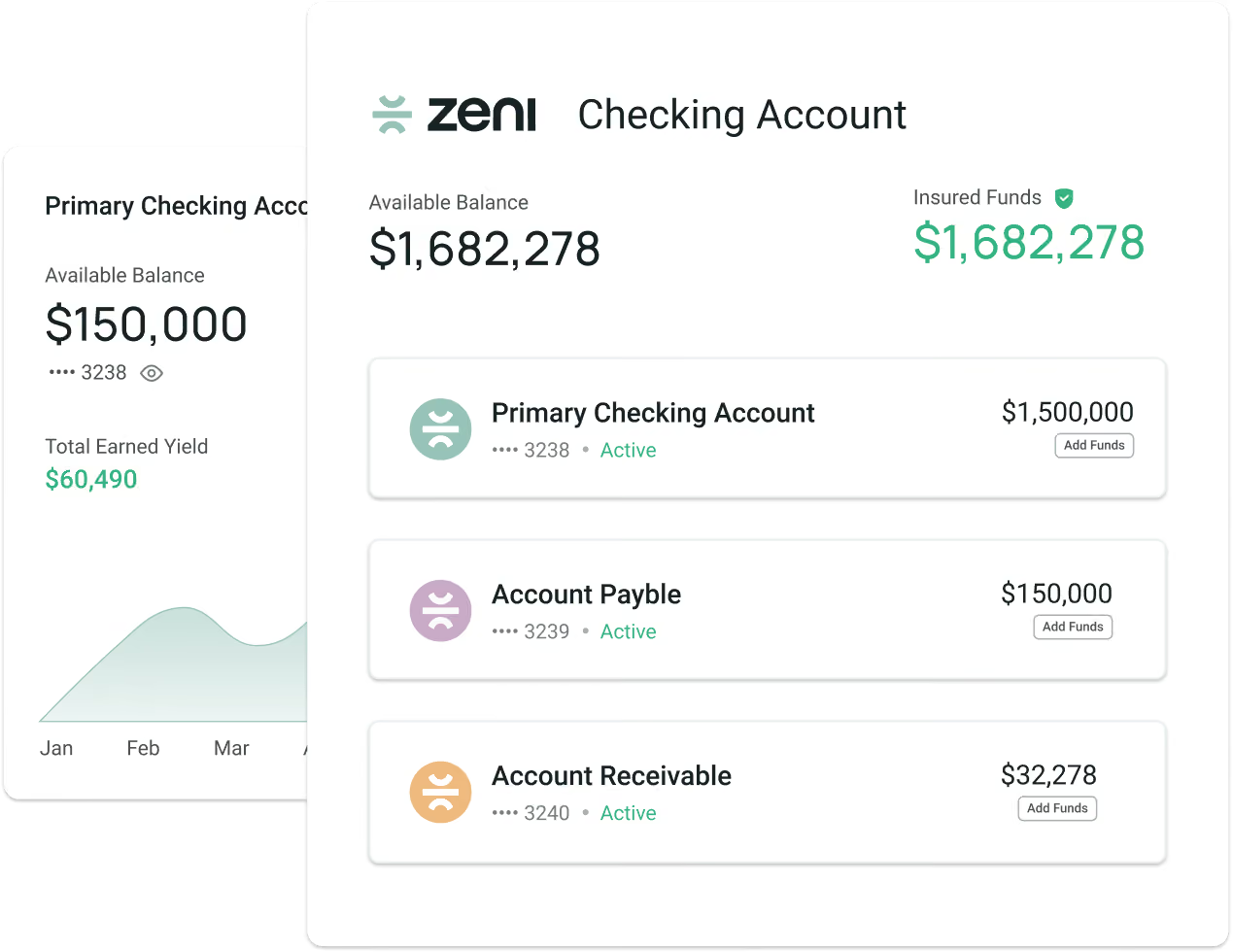

Zeni is a comprehensive financial management platform. It’s designed to help startups and small businesses eliminate the inefficiencies that come from juggling separate financial solutions.

In addition to our flagship bookkeeping, tax, and fractional CFO services, we offer a full suite of essential supporting products and services. These include bill payment software, business checking accounts, and payroll management.

We’ve built free ACH functionality into all three of these offerings, allowing you to pay vendors efficiently for no additional cost. Each feature is accessible through a single integrated dashboard and enhanced by the power of AI.

Learn more about Zeni ACH capabilities in the Business Checking, Bill Pay, and Employee Reimbursements products.

We picked Dharma because of their low monthly cost, low transaction fee, and processing tech offered to accept multiple versions of payments such as eChecks, credit cards, or paper checks. Dharma’s versatility is great for startups looking for an all-in-one payment processor.

Stripe is a well-known transaction platform with a robust transaction system. Stripe offers corporate credit cards and ACH payment processing services. Businesses at any stage can use.

stripe for ACH payments. However, Stripe has a list of prohibited businesses they do not service, all of which fall within the “high-risk” category. Unfortunately, clients aren’t always flagged as high-risk until after they begin using Stripe’s processes to accept payments, so be sure to ask about this prior to onboarding.

Payment cloud specializes in “high-risk” businesses (travel, for example). You don’t need to be in a high-risk group to use Payment cloud, but it's a plus for those who are. Dharma and Stripe refer clients they cannot support to Payment Cloud because of their ability to handle higher-risk businesses.

Merchants with a large percentage of card-not-present transactions are considered a higher risk. This is why other ACH processors like Dharma deny clients but refer over to PaymentCloud.

Small businesses, high-volume businesses, or startups aiming to expand benefit from using National Processing over larger platforms because of their pricing. They work with companies with low-processing rates while providing B2B services, but this ACH transfer service is ideal for employer-to-employee direct deposit.

Carat’s software supports world-recognized banks like Wells Fargo and Chase for easy international ACH payments. Carat’s mobile app makes it easy for businesses to one-step enroll their clients using their bank log-in for easy bank-to-bank transfers. Another cool feature is their customization options. You can create individual channels for ACH payments and eCheck acceptance based on your business needs.

Stax is another well-known processor that can be a good fit for businesses that process a minimum of $5,000 per month in transactions. With Stax, companies have the option to schedule recurring invoices and automate reminders for on-time payment consistency. As an all-in-one processor, Stax accepts eChecks, ACH payments, and others to make it easier for their clients to operate in a way that fits their business.

ACH stands for automated clearing house network run by the NACHA (National Automated Clearing House). ACH payments have been around since 1974 as an electronic payment method. ACH is a batch network processing system used by large financial institutions like banks to process large quantities of different transactions from one bank account to another.

Businesses use ACH processing systems when using direct deposit for payroll, and the IRS uses ACH for tax refunds and other government deposits. You can use ACH for recurring payments to cover operating and other business-related expenses.

ACH transactions and credit card transactions have two key differences to consider. ACH transactions have lower transaction costs compared to credit cards. ACH transaction fees remain around 1% or $.30 altogether.

Credit card processing runs on networks monitored by the card supplier, meaning there is a process of checking the card for the amount needed to trade. Once confirmed, the funds are guaranteed to be processed. ACH transactions are technically requests without a guarantee because they are sent in batches.

Non-guaranteed payments only affect a business if they are choosing to accept ACH customer payments. If you're considering paying vendors and other business expenses with ACH payments, the batch payment process shouldn’t be too big of a worry.

ACH payments are recorded in accounts payable or accounts receivable, depending on your company’s use of the ACH process. Each settlement needs to be accurately accounted for in your company’s books for a solid picture of your company’s financial standing.

Tax purposes: When tax time comes, the IRS will scrutinize your income to determine the amount of income tax owed. Issues with the IRS lengthen the amount of time you’ll receive your refund, if applicable, and can tie up other cash if you owe more to the IRS.

Vendor relationships: An error in the amount paid vs. the amount owed for expenses can result in late fees and a strained vendor relationship. If the error isn’t caught immediately, it can result in contract termination or higher fees that stack up over time.

Using traditional bookkeeping services means waiting on your books to be completed. We understand the importance of having a crystal clear view of your finances in real-time, so we created Zeni. Paired with an experienced team of controllers, our bookkeeping software gives you access to real-time financial data 24/7.

.webp)